Foresight 2024: "China's short video industry panorama map" (with market size, competitive landscape and development prospects, etc.)

Release time:

2024-05-23 16:04

Source:

-- Original title: Foresight 2024: "China's short video industry panorama map in 2024" (with market size, competition pattern and development prospects, etc.)

Major listed companies in the short video industry: Fast Hand (01024.HK), Tencent (00700.HK), Baidu (09888.HK), bilibili(09626.HK), etc.

The core data of this article: short video industry user size; short video industry market size; number of MCN institutions; short video advertising revenue.

Industry Overview

1. Definition and classification

Short video is a short video, which is a way of transmitting Internet content. It is generally a video with a duration of less than 5 minutes transmitted on new media on the Internet. Short video content combines skills sharing, humor and funny, fashion trends, social hot spots, street interviews, public welfare education, advertising creativity, business customization and other topics. Due to the short content, it can be a separate piece or a series of columns.

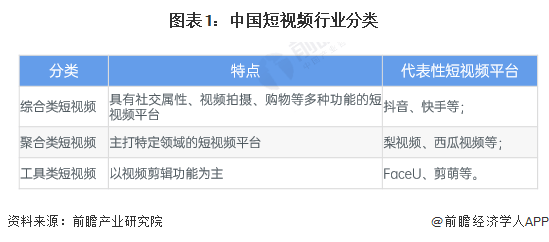

Short video products can be divided into comprehensive short video, aggregate short video and tool short video. Comprehensive short video generally refers to a short video platform with social attributes, video shooting, shopping and other functions. Representative products include tremolo and fast hands. Aggregation short video focuses on short video platforms in specific fields, such as pear video and watermelon video. Tool short video refers to short video platforms that mainly focus on video editing functions, such as FaceU and Climb Meng.

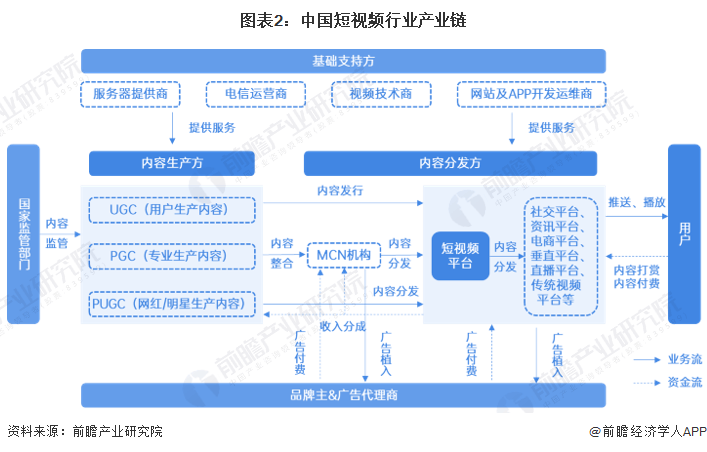

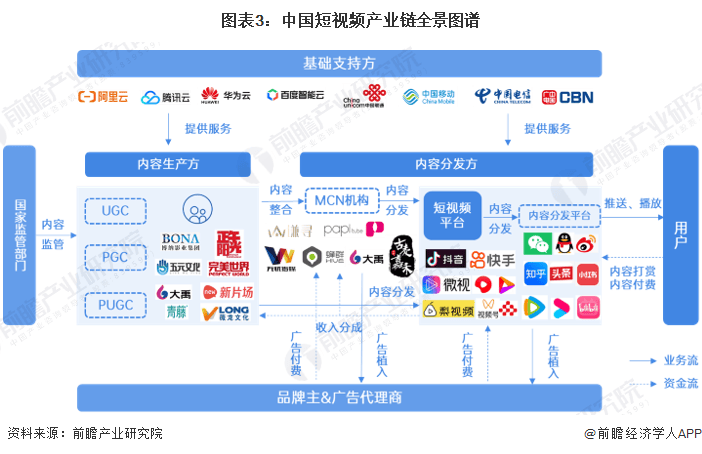

2, industrial chain analysis: industrial chain links diversified.

China's short video industry chain mainly includes upstream content producers, midstream content distributors and downstream user terminals. Upstream content producers are mainly divided into three categories: UGC (user-produced content), PGC (professional-produced content) and PUGC (online red/star-produced content); midstream content distributors include short video platforms, social platforms, News platforms, e-commerce platforms, vertical platforms, live broadcast platforms and traditional video platforms. In addition, the industry chain participants also include basic support parties (such as server providers, telecom operators, technology operators, etc.), advertisers and regulatory authorities.

At present, the short video upstream content producers mainly include Boehner Pictures, Noon Sunshine, Five Yuan Culture, Dayu Network, New Film Field, Green Rattan Culture, Wei Long Culture and so on. There are many participants in the distribution of short video content. Mobile short video APP includes trembles, fast hands, Tencent microvision, watermelon video, good-looking video, pear video, WeChat video number, CCTV frequency, etc. Content distribution platforms mainly include social applications such as WeChat, QQ, Sina Weibo and Little Red Riding Book, and information platforms such as Zhihu and Today's Headline. In addition, traditional video platforms also cover short video content distribution, such as Tencent video, Youku video, beep mile and so on. Short video basic supporters mainly include Aliyun, Tencent Cloud, Huawei Cloud, Baidu Smart Cloud, China Unicom, China Mobile, China Telecom and China Radio and Television.

Industry development history: layout of more enterprises, the industry into a stable period

The short video industry sprouted in 2011. Kuaishou, Weishi and Meipai were all early participants. After that, driven by the development of smart phones, mobile Internet and 4G technology, the industry developed rapidly. In 2016, the powerful algorithm recommend mechanism provided users with a large amount of high-quality short video content, and the scale of advertising realization grew rapidly. In recent years, the short video industry has formed a "two strong" competition pattern of shaking sound. Due to the deepening trend of video content, social platforms such as WeChat, Weibo and Little Red Riding Book have also added short video functions, further enhancing the penetration rate of short videos.

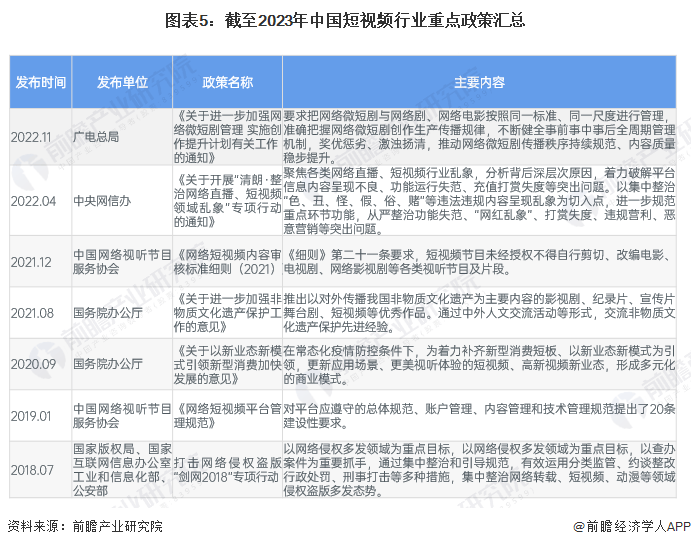

Industry policy background: focus on industry chaos, strengthen industry supervision

Under the background of the gradual growth of short video users in China, the low entry threshold of short video and the lack of self-censorship mechanism have created a large number of vulgar content, the proliferation of false content and the problem of content plagiarism. To this end, China has stepped up the supervision of the short video industry.

In recent years, various government departments have issued a series of policies and regulations to promote the healthy and orderly development of the domestic short video industry and other related video industries. The relevant policies, regulations and main contents are shown in the following table:

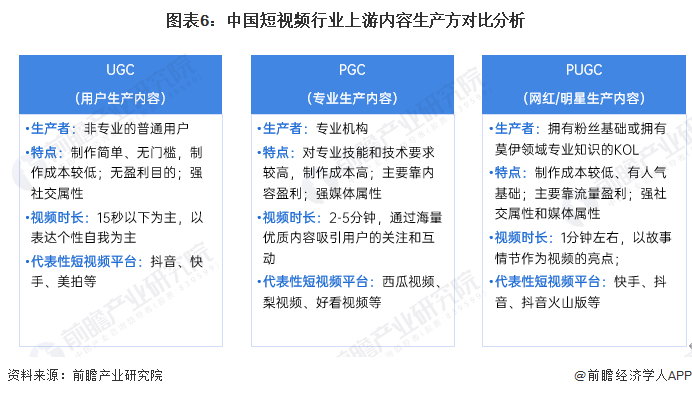

Upstream content producers: three categories of content producers (UGC, PGC and PUGC)

At present, content producers in the short video industry include UGC (user-produced content), PGC (professional-produced content) and PUGC (online red/star-produced content).

UGC producers are non-professional ordinary users. This kind of group has low cost and simple production, so there is basically no threshold and has strong social attributes. UGC producer content production mainly to express individual self-oriented, the general production time is less than 15 seconds, the representative platform has a sound, fast hand and beautiful beat.

PGC producers are professional organizations, which have higher production costs, professionalism and technical requirements than the other two types of producers. They have strong media attributes. They take 2-5 minutes to produce short videos. They generally attract users' attention and interaction through massive high-quality content. Generally, these people are active in short video platforms such as watermelon videos, pear videos and good-looking videos.

PUGC producers are KOLs with a fan base or expertise in a particular field, which are low-cost, rely heavily on traffic for profit, and have both social and media attributes. Generally, this kind of content producers produce videos for about 1 minute, mainly with the storyline as the highlight of the video. Fast hand, shake sound, shake sound volcano version for this group of people's preferred short video production platform.

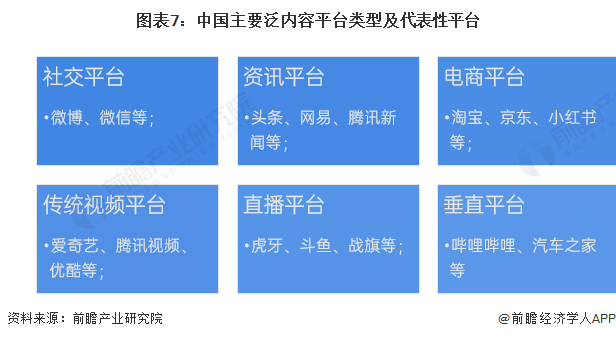

Downstream pan-content platforms: numerous and rich in types

Since its development, China has formed various types of pan-content platforms, including social platforms, information platforms, e-commerce platforms, traditional video platforms, live broadcast platforms, vertical platforms, etc. Social platforms include microblog, WeChat, etc. Representative information platforms include headlines, Netease, Tencent news, etc. E-commerce platforms include Taobao, Jingdong, Little Red Riding Book, etc. Traditional video platforms include Aiqiyi, Tencent Video, Youku, etc.

Industry development status

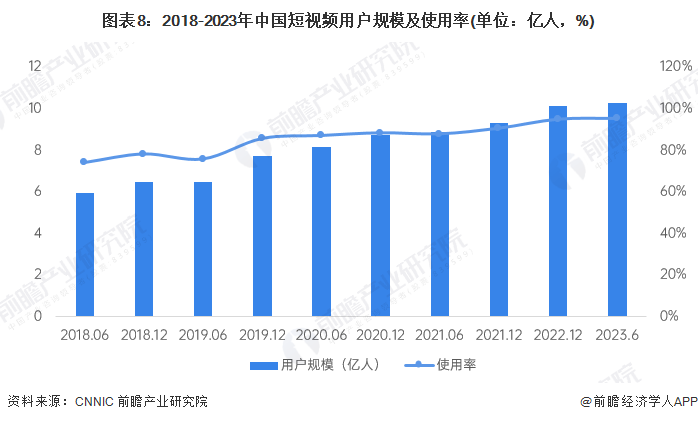

1. The number of users exceeds 1 billion

Short video length, content concentration, strong expression, in line with the fragmented viewing habits, deep penetration into the daily life of the public. At the same time, short videos meet the needs of personalized and video-based expression and sharing, and more and more user groups shoot/upload short videos.

The latest data released by the China Internet Network Information Center CNNIC shows that from 2018 to 2023, the scale of short video users in my country continued to grow. As of June 2023, the number of short video users in China reached 1.026 billion, another record high, and the user usage rate increased to 95.2.

Note: Usage rate = short video user size/netizen user size.

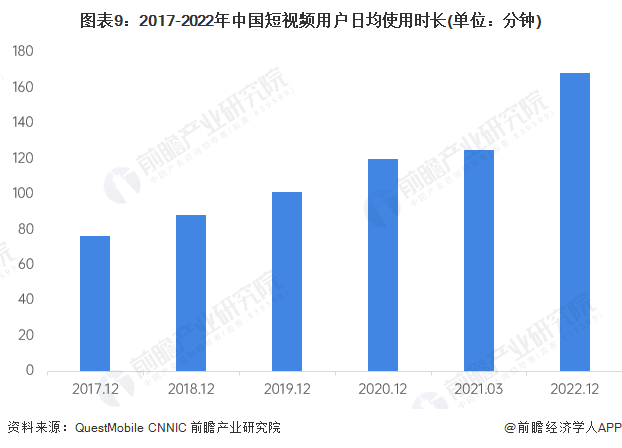

2, user stickiness continues to improve

At the same time, the length of time users use short videos is also increasing. In terms of per capita single-day usage time, the per capita single-day usage time of short videos in China continues to grow. According to CNNIC data from the China Internet Network Information Center, as of December 2022, the per capita single-day usage time of short videos in China is 168 minutes, and the stickiness of short video users continues to increase.

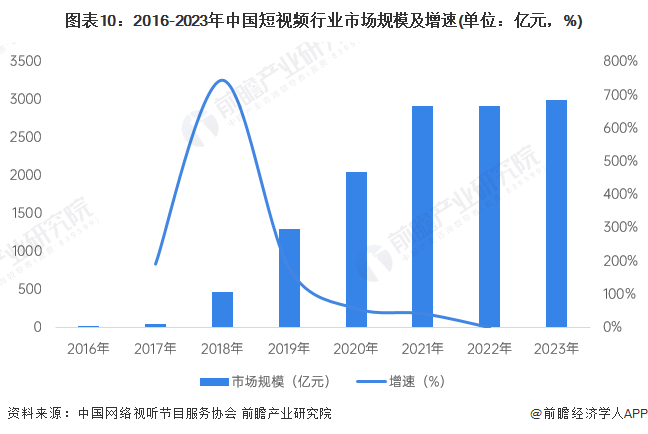

The market size is around 0.3 billion.

With the continuous growth of user scale and usage time, China's short video platforms are also actively exploring more diversified and deeper commercial realization models. The short video industry is booming and the market scale is growing at a high speed. According to the data released by the China Network Audiovisual Program Service Association, the market size of China's short video industry will exceed 290 billion yuan in 2022. Preliminary statistics 2023 market size in 300 billion yuan.

Note: 2023 is a preliminary statistic, subject to official release at that time.

industry competition pattern

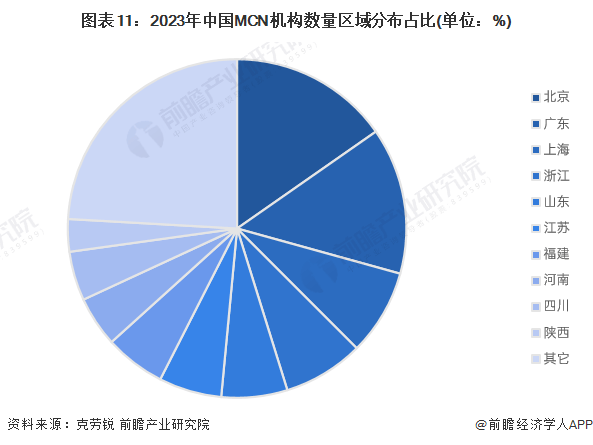

1, regional competition: MCN institutions are mostly distributed in first-tier/new first-tier cities, Beijing is the most

Since 2017, China's MCN industry has seen explosive growth. At present, China's MCN industry mainly has seven types of formats, with content production and operation formats as the basic core, and the other five formats-marketing formats, e-commerce formats, brokerage formats, community/knowledge payment formats and IP licensing formats as the extension of realization, combined to seek differentiated development.

In recent years, MCN institutions have blossomed everywhere in China. Crowley research data show that in 2023, China's MCN institutions are mostly located in first-tier/new first-tier cities. Among them, Beijing accounted for the largest proportion, more than 15%, followed by Guangdong and Shanghai, respectively, 14% and 8.2. On the whole, except for Beijing, which has the characteristics of the capital, MCN companies are mostly distributed in the eastern coastal areas of my country, mainly concentrated in the more economically developed provinces and cities.

Note: The above data are from the Crowley 2023 MCN Institutional Survival Survey, with a survey period of December 2022-February 2023 and a total sample size of N = 600.

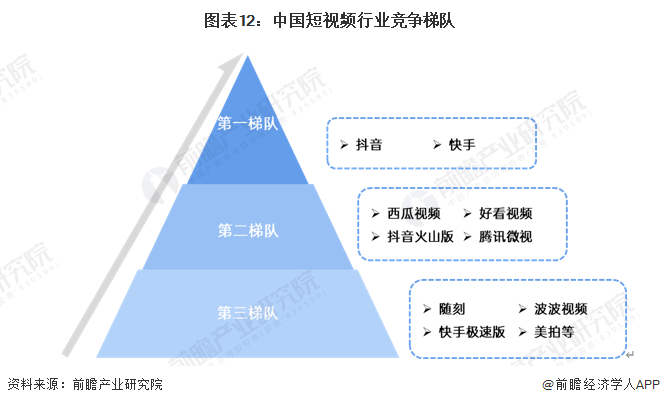

2, enterprise competition: the competitive landscape is stable, the platform factions bloom.

As a mainstream Internet application, the market competition pattern of short video industry is relatively stable. Shake short videos and fast short videos are firmly in the first echelon of the industry. Byte Beat's Watermelon Video, Shake Volcano Edition, Baidu's Good-looking Video, Tencent's Micro Vision is in the second echelon; Short video APP such as Aiqiyi, Fast Hand Speed Edition, Bobo Video and Meipai is in the third echelon. From a dynamic development perspective, the second tier of user usage has increased significantly.

At present, China's short video industry competition factions mainly include today's headline system, Tencent system, fast hand system, Baidu system, Sina system, Ali system, Meitu system, B station system, 360 system and Netease system, short video platform factions present a hundred flowers bloom situation. Among them, one of the most popular video platforms-shaking sound belongs to today's headline system.

Industry development prospects and trend forecast

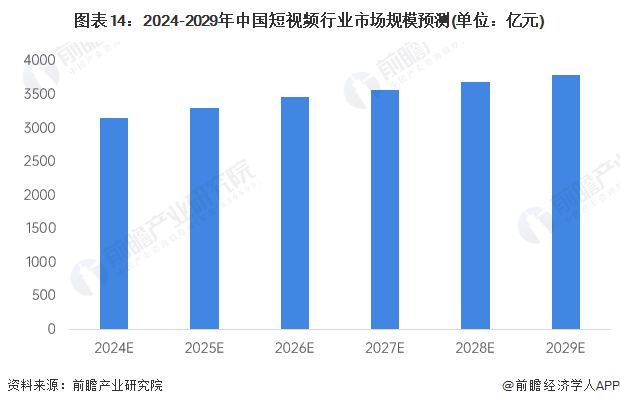

1. Development Prospect: The market size of short video industry will be close to 380 billion yuan in 2029

In the future, the short video platform will further seek new breakthroughs, such as joining live broadcast, e-commerce and other businesses. At present, the head short video platform is already developing online live broadcast business, and seeks to deepen the relationship with other content creators, while developing new functions to deepen the interaction between creators and users. The increase in 5G penetration, artificial intelligence and the development of big data technology will provide new support for short video platforms. In addition, the state has strengthened the supervision of the industry, and the platform has also strengthened the review of short video content released by users. On the whole, the short video industry has great potential for development. It is preliminarily predicted that by 2029, the market size of China's short video industry will be close to 380 billion yuan.

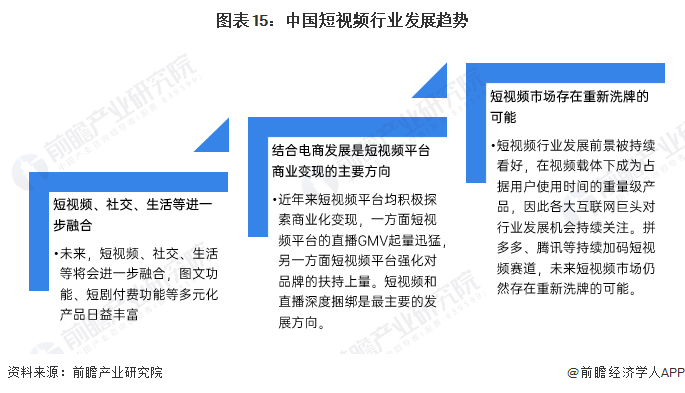

2. Development trend: short video, social and life will be further integrated in the future

In the future, short video, social and life will be further integrated. At the same time, short video platforms are actively exploring commercial realization, and combined with the development of e-commerce is the most important direction. The development prospects of the short video industry continue to be optimistic, under the video carrier to become a heavyweight product that occupies the user's time, spell more, Tencent and other continuous plus code short video track, the future short video market still has the possibility of reshuffling.

For more research and analysis of this industry, please refer to the "China Short Video Industry Market Prospect Forecast and Investment Strategic Planning Analysis Report" by the Prospective Industry Research Institute.

At the same time, the Prospective Industry Research Institute also provides solutions such as industrial big data, industrial research reports, industrial planning, park planning, industrial investment promotion, industrial mapping, intelligent investment promotion system, industry status certificate, IPO consultation/investment feasibility study, specialized and special new small giant declaration, etc. Citing the contents of this article in any public disclosure such as the prospectus and the company's annual report requires formal authorization from the Prospective Industry Research Institute.

Related News